Financing in a Rising Rate Environment

How do you approach financing when interest rates are rising?

By: Marc Stern | Chief Lending Officer

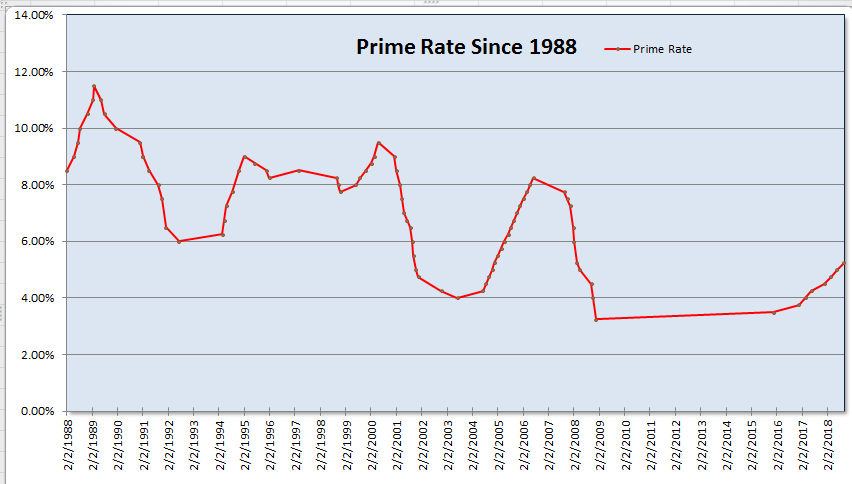

After more than 8 years of historically low interest rates, the economy is starting to heat up and interest rates are going up. How do you handle this when seeking financing to grow or establish your business? First, let’s look at the growth in interest rates. There have been 4 quarter point increases in the prime rate over the past year. There are more increases forecast for 2019.

When Interest Rates Go Up, You Pay More.

Higher interest rates mean you pay more to borrow money. Rising interest rates don’t always signal bad things, however. They can be a sign of a healthy, growing economy and a time in which starting or expanding your business might be a good idea. One thing to remember is that in a rising interest rate environment, if you do not borrow now, you may be setting yourself up to pay more later.

Navigating the Rising Rates

You can navigate the rising interest rate landscape by utilizing some of the following strategies and tips:

- Refinance existing loans – While your new rate may be higher your payments most likely will be lower. This is achieved through an extension of the loan term.

- Increase your creditworthiness. In other words, keep your credit score high. Doing so may reduce the cost of your borrowing

- Lock in rates on projects. Delaying financed projects may result in higher rates later in this environment.